Financial Stress at Work: Why What Employees Don’t Know Is Costing You Money

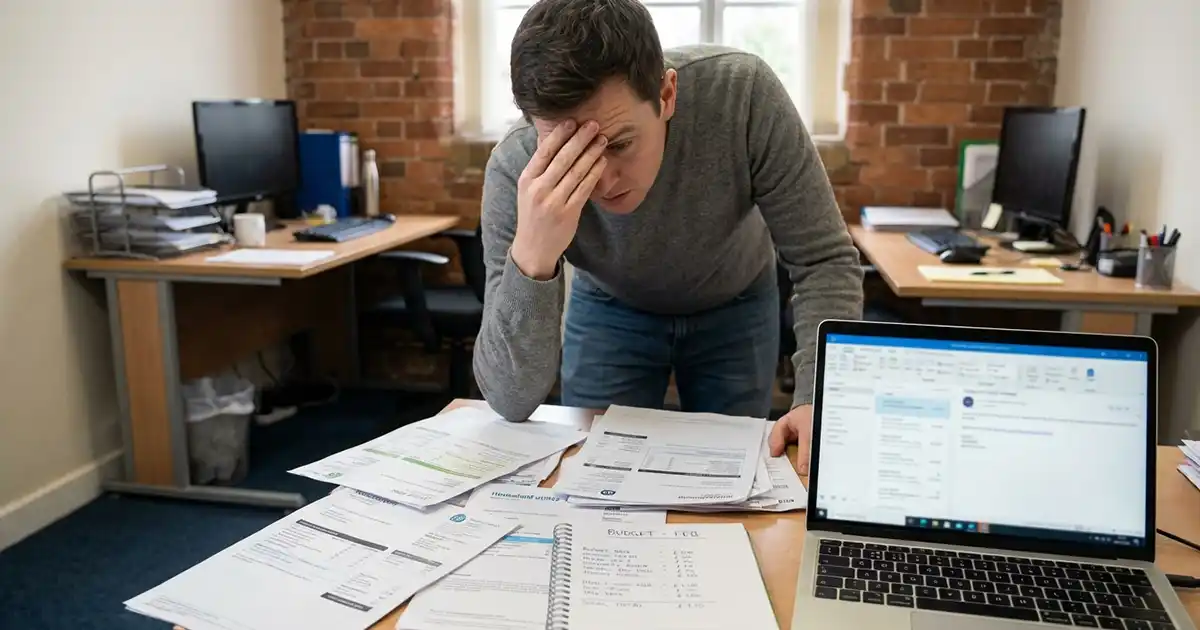

There’s a stat doing the rounds in HR circles at the moment that tends to get people’s attention. According to HR Magazine, employees are losing roughly a week of productive working time every year because of financial stress. A whole week. Per person. And separately, Employee Benefits has reported that around two-fifths of employees say money worries are actively dragging down their performance at work.

If you run an SME or hold any HR responsibility in a larger organisation, those numbers should give you pause - not because they’re surprising, but because they point to a problem most employers have quietly accepted as someone else’s to solve.

It isn’t.

This Isn’t Just About What People Earn

The instinct, understandably, is to frame financial stress as a pay issue. Cost of living is high, wages haven’t kept pace, and there’s a limit to what any employer can do about macroeconomic conditions. Fair enough.

But pay is only part of the picture. A significant chunk of financial anxiety in the workplace has nothing to do with income levels; it comes from not understanding how money works. Pensions, tax, National Insurance, debt, savings. For a large proportion of employees, these subjects are genuinely confusing, and that confusion breeds anxiety.

Think about workplace pensions alone. Most employees are enrolled in one. Plenty couldn’t tell you what their employer contributes, how the tax relief works, or what they’re actually invested in. Some don’t even know they can change their contribution. An employer might be putting in 5%, 6%, 8%, and the employee treats it as background noise because they don’t understand what it means for their future. That’s a valuable benefit being quietly wasted, on both sides.

Industry reporting has highlighted the persistent gap between the benefits employers offer and employees’ actual awareness of them. Education, not generosity, is often the missing piece.

What It’s Actually Costing You

Lost productivity is the obvious headline, but the full picture is messier than that. Financial stress doesn’t just make people slower — it makes them distracted, withdrawn, and more likely to take sick days they might not otherwise have taken. In a small team, one person operating at 70% capacity has a ripple effect that’s hard to quantify but very easy to feel.

Presenteeism (showing up physically while mentally somewhere else entirely) is notoriously difficult to measure, which is probably why it gets underestimated. But if someone is sitting at their desk running through a debt repayment problem in their head, they’re not doing their job. Not fully, anyway.

Retention is part of this too. Employees who feel financially insecure are more likely to job-hop in search of a pay rise, even when the rest of their package is strong. Losing a decent member of staff and replacing them costs far more than most employers account for when it actually happens.

What You Can Actually Do About It

This is where it gets practical. Employers can’t give regulated financial advice. And nor should they try. But there’s a meaningful difference between giving advice and providing education, and it’s a distinction worth understanding.

Financial wellbeing education means helping employees get to grips with how things work: how their pension operates, how tax is calculated, what an emergency fund is and why it matters, how to think about debt. None of that requires financial services authorisation. It’s information, not instruction. Employees can then take that knowledge and seek personalised advice from a regulated adviser if they need it, but they’ll go into that conversation with a much clearer head.

The format matters too. One-off seminars sound nice but rarely change behaviour. People dip in, nod along, and forget most of it by Thursday. Digital learning done well works differently. Employees can go at their own pace, revisit topics when their circumstances change (a new mortgage, a promotion, approaching retirement), and actually absorb information without the social pressure of a group setting. Completion rates are trackable. Knowledge gaps become visible. It scales without much additional effort from whoever’s managing it.

For an SME owner wearing five hats, that last point matters a lot.

What Good Financial Education Actually Covers

There’s no universal syllabus, but certain topics come up again and again as areas where employees feel underserved:

- Workplace pensions: how contributions work, what auto-enrolment means, the basics of investment risk

- Budgeting: not in a patronising way, but practical tools for managing irregular income or unexpected expenses

- Tax and National Insurance: most people have a rough sense of this but surprisingly few understand it properly

- Emergency savings: the why, the how much, and the practical psychology of actually building one

- Debt: the difference between manageable and problematic, and how to start addressing the latter

- Long-term planning: retirement, yes, but also broader financial resilience

None of this is glamorous. But for an employee who’s never had anyone explain how their payslip actually works, or what happens to their pension if they leave their job, it can be genuinely useful, and genuinely reassuring.

A Note on the SME Reality

Large organisations have reward teams, HR business partners, and procurement budgets for this sort of thing. Most SMEs don’t. If you’re reading this as someone who handles HR as part of a broader role - or as the business owner who ends up dealing with everything - you’re probably not looking for a complex, bespoke programme. You want something that works, doesn’t require significant ongoing management, and actually helps your people.

That’s the gap Aspina is working to fill. We’re building structured, straightforward e-learning content on financial wellbeing topics, written for employees rather than financial specialists. It’s early days, but if you’re thinking about this for your organisation and want to know more, we’d be glad to talk.

The reporting on financial stress at work isn’t new, but it’s becoming harder to ignore. A week of lost productivity per employee, per year, adds up fast — and the fix isn’t necessarily a pay rise. Sometimes it’s just helping people understand the financial picture they’re already in.

That’s something employers can actually do something about.